The 5 Backtesting Mistakes That Make Strategies Look Profitable (But Aren't)

Discover the 5 most common backtesting mistakes that make trading strategies look profitable when they're not — overfitting, look-ahead bias, missing costs, and more.

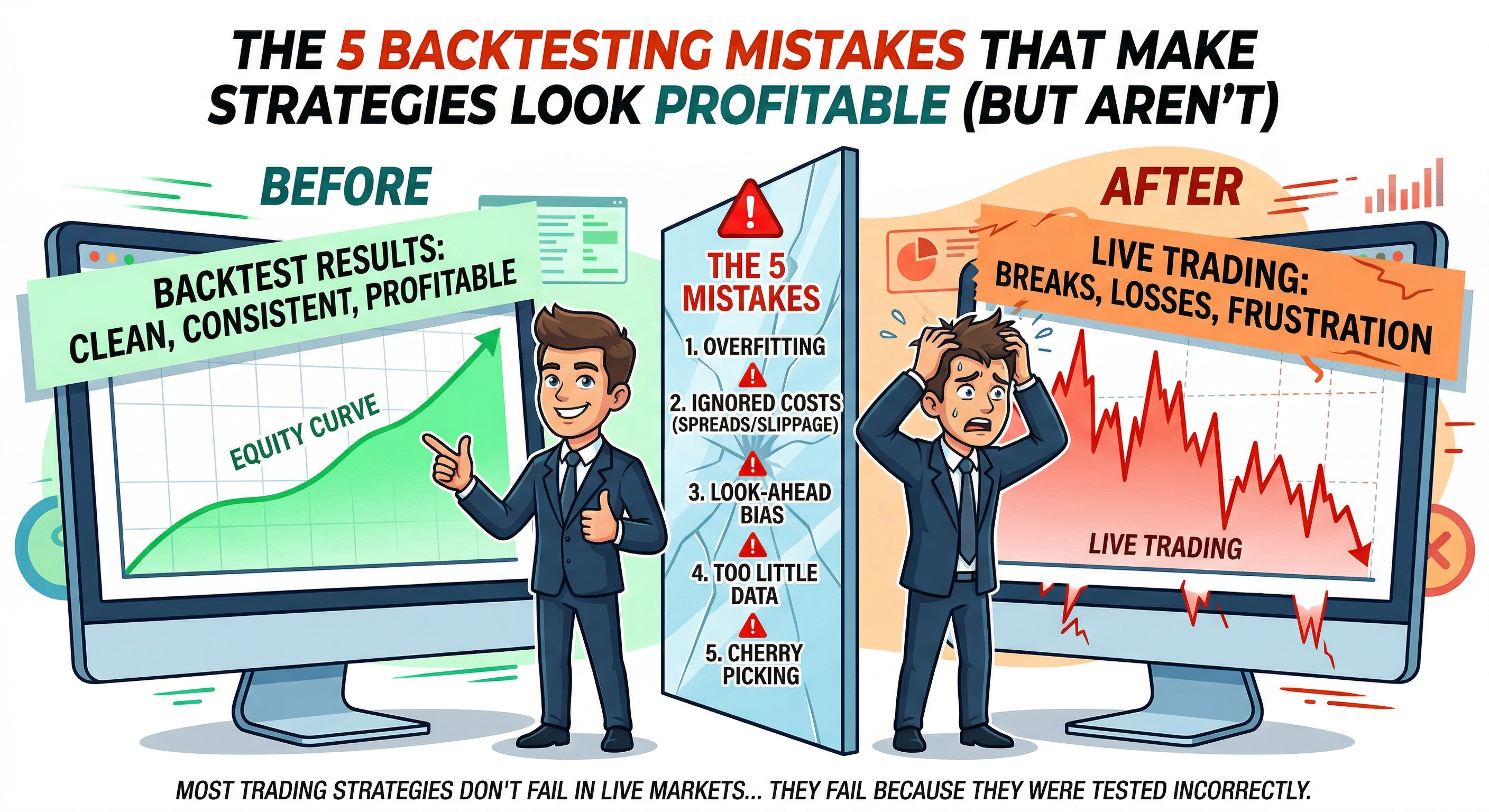

Most trading strategies don't fail in live markets… they fail because they were tested incorrectly.

You run a backtest. The results look clean. Profitable. Consistent. Then you trade it live — and it breaks.

If that's happening, the problem is usually not the market. It's your backtesting process.

In this article, we'll break down the 5 most common backtesting mistakes that make strategies look profitable — when they're not.

Why Most Backtests Are Misleading

Backtesting is supposed to answer one question: Does this strategy actually have an edge?

But if your testing process is flawed, you're not measuring an edge. You're measuring an illusion.

Let's fix that.

1. Overfitting (The Most Dangerous Mistake)

Overfitting happens when you optimize your strategy so much that it perfectly matches past data — but only that data.

You tweak parameters again and again:

- indicator settings

- entry conditions

- filters

Until the equity curve looks perfect.

But here's the reality: you didn't find an edge. You forced the strategy to fit the past.

A robust strategy should work across:

- different time periods

- different market conditions

- multiple instruments

If it only works on one dataset, it's likely overfitted.

2. Ignoring Trading Costs

Backtests often assume perfect execution. Real trading doesn't.

Every trade includes:

- spreads

- commissions

- slippage

These costs can completely change your results — especially for:

- scalping strategies

- high-frequency systems

- low risk-reward trades

A strategy that looks profitable on paper can become breakeven — or worse — once realistic costs are applied.

If you're not including costs, your backtest is incomplete.

3. Look-Ahead Bias (Fake Precision)

Look-ahead bias happens when your strategy uses information that wasn't available at the time.

Common examples:

- entering based on candle close before it actually closes

- indicators that repaint signals

This creates "perfect" entries in backtests. But those entries never existed in real time.

The result? A strategy that looks highly accurate… but can't be executed live.

4. Too Little Data (False Confidence)

Small sample sizes create false confidence.

Example: 20 trades, 15 winners. Looks great. But statistically, it means almost nothing. Random results can look consistent over small samples.

To properly evaluate a strategy, you need:

- hundreds of trades

- across different market conditions

Without that, you're making decisions based on noise.

5. Cherry Picking Trades

This is common in manual backtesting. You scroll through charts and select clean setups and obvious entries — but skip messy conditions, borderline trades, and losing examples.

This creates a biased dataset. Your results only reflect the best-case scenario. Real trading doesn't work like that.

If your rules aren't objective and repeatable, your backtest results won't match reality.

How to Backtest Like a Professional Trader

If you want your results to actually mean something, focus on this:

- Use strict, objective rules — no guessing, no interpretation

- Test large sample sizes — at least 100–300 trades

- Include real trading conditions — spreads, commissions, slippage

- Track every trade — this is where most traders fail

Without structured tracking, you can't analyse performance, find weaknesses, or improve your strategy.

The Missing Piece: Trade Tracking

Backtesting gives you potential. Tracking gives you truth.

If you're serious about improving, you need a system to log every trade, review your execution, and measure real performance over time.

That's exactly why Treydly exists.

Treydly is a trading journal designed to help you:

- track every trade in a structured way

- analyse your strategy performance

- identify mistakes and patterns

- improve consistency over time

If your goal is to move from random results to controlled performance, structured trade tracking is the step most traders are missing.

Start tracking your trades with Treydly →

Final Thought

A clean backtest doesn't mean a profitable strategy. It just means your data looks good.

What matters is whether your edge survives real execution, real costs, and real market conditions.

Fix your backtesting process… and your results will start to reflect reality.

Track this in Treydly — free

Connect your MT5, MT4, or cTrader account, import your trade history, get all your statistics instantly.

Create Free Account